Why Should Investors Clarify Goals Before Renting or Selling a Property?

Imagine selling a property, only to find out 20 years later that it would have doubled or tripled in value. For investors, it often doesn’t take much—just a harsh winter in Southeastern Wisconsin and rising maintenance headaches—to make this costly mistake. But if you’re wondering whether to sell now or hold for the long-term, here’s how to make that decision with confidence.

Investors deciding whether to rent or sell should start by asking, why. Managing properties for thousands of investors for nearly two decades has taught us at Performance Asset Management (PAM) that the answer is often tied to financial freedom. Whether that’s retirement security, family flexibility, building funds for education, or providing for charities, it all depends.

Clarifying the why helps investors better identify the temporary discomforts of stress, uncertainty, and responsibilities, allowing them to anchor decisions in hard data and market performance. Whether you decide to continue to rent or sell your property, keep reading for an unbiased comparison that will help you decide which approach is best for you.

Full disclaimer: As a property management company, we acknowledge the potential for bias. Instead of advocating renting or selling, our goal is to present objective data and a framework to guide informed decisions. Because every investor has a unique situation, both options should be evaluated carefully before making a final choice.

How Should Investors Evaluate Rental Cash Flow Before Deciding to Rent or Sell?

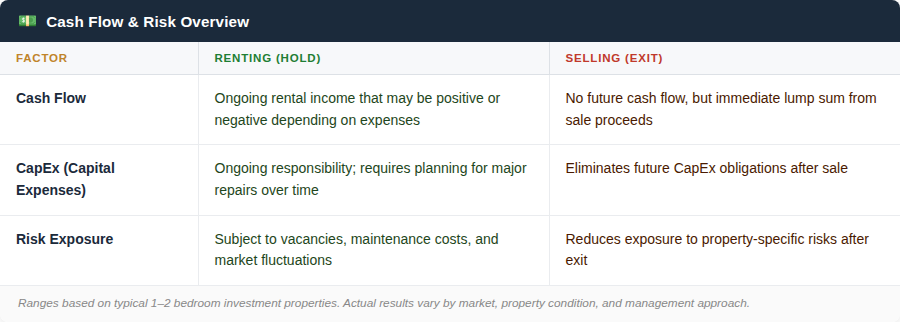

Before deciding to rent or sell, investors should evaluate rental cash flow by measuring if that amount can reliably support their lifestyle, risk tolerance, and long-term goals.

Because over time, plans change, and life happens. Property investment is hardly an exception to that general rule of life. Investors considering whether to rent or sell should avoid only evaluating monthly rental cash flow and consider a broader financial approach.

Negative cash flow is hardly ideal, but it is usually manageable depending on lifestyle choices, such as income stability and expense structure. Use lifestyle math to combine earned income, living expenses, emergency reserves, and investment obligations into one realistic picture. This allows investors to anticipate potential cash flow pressures before they actually happen.

Factors like job changes, family concerns, or health problems can influence how well an investor handles financial ups and downs. With the CapEx formula, investors can better identify cash flow pressures. And by anticipating those expenses, they can react to them decisively, instead of emotionally responding to negative events that drain their cash flow.

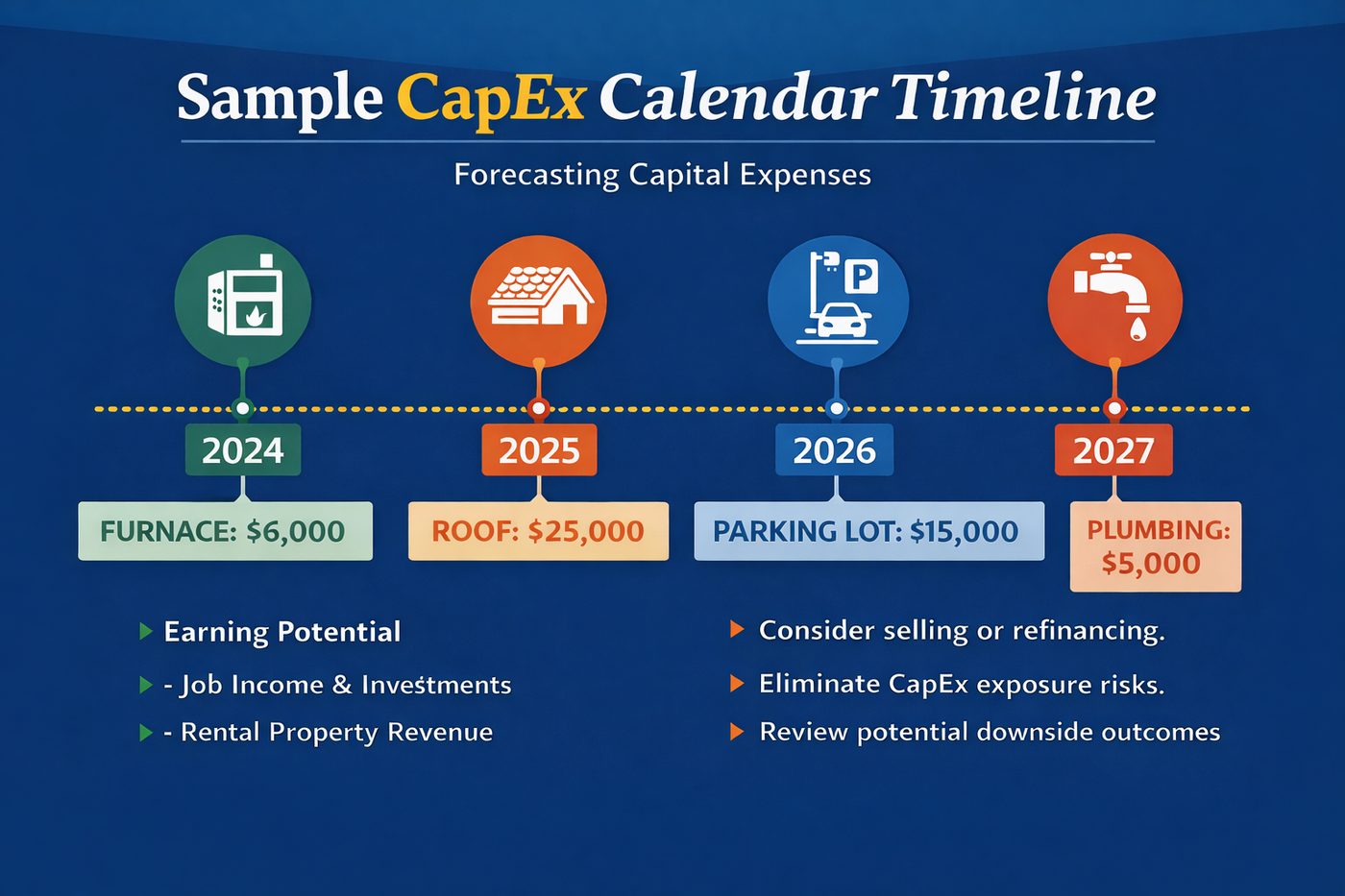

Reviewing a CapEx Formula Timeline for Property Investors

For example, if an investor owns a small multifamily property where the rent covers the mortgage, the units are occupied, even though nothing feels urgent, major systems are aging:

A furnace that’s been running for decades can finally give out.

The following year, an inspection reveals the roof is nearing the end of its life.

Another year later, resurfacing the parking lot becomes unavoidable because deferred maintenance would be a liability.

Around the same time, a plumbing failure happens, though small on its own, it turns out to be costly when combined with everything else.

None of these expenses are unusual. In fact, they’re predictable. The problem isn’t the costs themselves—it’s encountering them back-to-back without a plan.

That’s why experienced investors don’t look at capital expenses as one-off surprises. They map them out over time, estimate potential exposure, and decide in advance whether the property aligns with costs that may realistically occur over several years. Forecasting these kinds of factors early on can be crucial for achieving long-term growth and avoiding rushed decisions.

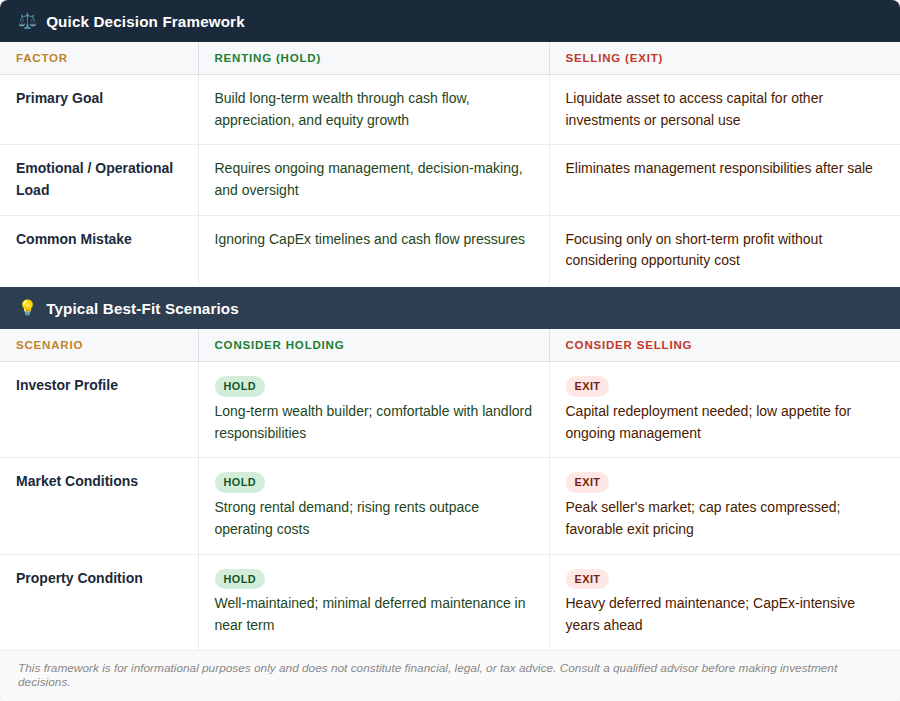

What Helps Property Investors Decide Whether to Rent or Sell?

Aligning long-term goals, cash flow needs, and risk tolerance with performance metrics such as IRR, CapEx timelines, and market conditions is typically the best strategy for investors deciding between holding or selling.

The common investor mistake in terms of deciding whether to rent or sell is focusing on short-term gains by thinking, “If I sell, I’ll make $50,000,” without accounting for long-term opportunity costs. That fails to address how much that property could have earned over 20 or more years.

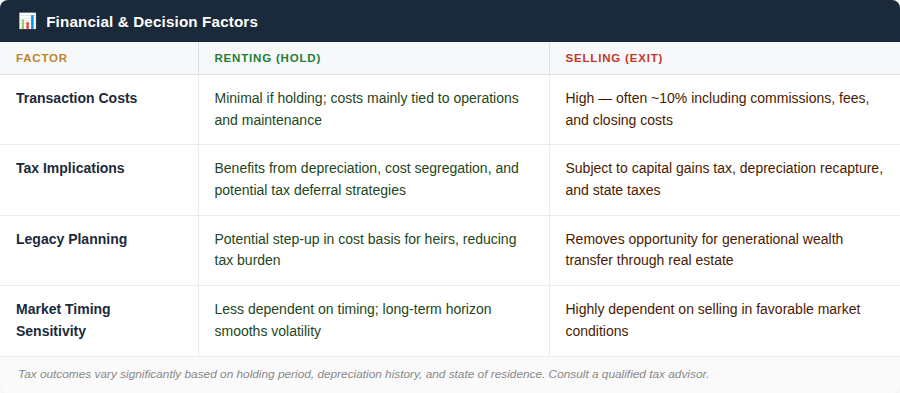

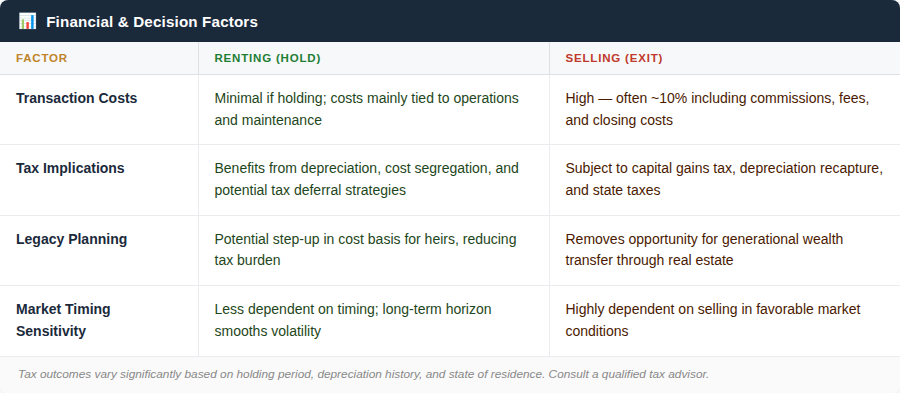

Transaction Costs

Investors also underestimate transaction costs. Because real estate involves commissions, loan origination fees, title fees, and property upgrades, on purchase and sale combined, costs can approach around 10%. Thinking of property the same way a trader works with stock ignores realities.

Taxes

Taxes are another major, oftentimes misunderstood component of selling. Holding a property longer than 12 months typically shifts taxation from ordinary income rates to capital gains rates, though depreciation recapture and state taxes can still significantly affect net proceeds.

Strategies like cost segregation and bonus depreciation can significantly affect monthly and annual cash flow, reinforcing how tax planning often shapes the decision to sell or hold.

For investors focused on legacy planning, it’s also important to understand that real estate typically receives a step-up in cost basis at death, potentially allowing heirs to inherit the property at current market value and reduce or eliminate prior capital gains exposure.

Market Conditions

While buying and selling frequently erodes returns due to commissions, financing fees, and closing costs, market conditions matter too. Markets in favor of sellers can materially increase exit value. Poorly performing properties, due to the asset or the neighborhood, benefit from objective evaluation.

How Does an Investor’s Timeline Impact Renting vs. Selling?

An investor’s timeline impacts whether renting or selling a property makes sense, with longer-term horizons often favoring holding for appreciation and stronger returns.

Investors who use exit timelines to guide their strategies are often better equipped to handle the fluctuations in real estate performance over time, as longer horizons can help investors earn more from their initial investment because of the following reasons:

Appreciation: The market value of a property typically increases over time, making it advantageous to hold onto an asset due to higher future sale prices.

Debt paydown: Making mortgage payments decreases the loan balance, increasing ownership equity in the property.

Compounding returns: Rental income and reinvested profits grow over time, generating even more wealth as gains build on previous gains.

Internal Rate of Return (IRR) provides a more accurate long-term perspective than simple ROI, as issues with short-term cash flow look different when analyzed over two or more decades. Some investors underestimate how much property value can grow over time, focusing on short-term stress, which can lead to sacrificing long-term wealth creation.

A Smarter Rent vs. Sell Strategy, Backed by PAM’s Investor Framework

Choosing to rent or sell is rarely a simple decision. Finding the right answer depends on goals, timelines, lifestyle, and risk tolerance. Data-driven decisions and objective frameworks can reduce reactive decisions.

At PAM, these decisions are guided by reports that reframe cash flow, appreciation, and equity growth over time, so investors can see the full financial picture and gain confidence in their decisions by understanding what they could potentially be giving up.