How to Decide Whether to Rent or Sell: A Framework for Investors

Homeowners often find themselves at a crossroads between renting or selling. Their end goal is achieving the best long-term ROI. But before taking steps, they need to know if renting is even affordable. Then, it’s possible to see the wealth waiting at the end of the renting route. The challenge for them is understanding that renting typically outperforms when affordability exists.

Without a clear process, owners risk choosing short-term liquidity over long-term performance potential. Investors who bridge the gap between today’s affordability and tomorrow’s growth build a powerful investment tool that can outperform most retirement plans. However, it takes the right mathematical tools to understand that fact and the math behind measuring returns.

At Performance Asset Management (PAM), we leverage nearly 20 years of experience supporting investors with deciding whether to rent or sell. The best long-term decision depends on affordability, time horizon, and total return potential. Keep reading to learn how to build a structured framework, eliminate emotional bias, and improve clarity in decision-making.

Full disclaimer: We acknowledge the potential for bias, as we are in the business of aiding investors with managing investments. This article is designed to help you make the right decision for your future, whether it is through renting or selling.

Can You Afford to Hold the Property as a Rental Month-to-Month?

If holding the property is affordable, renting becomes viable; if not, selling reduces risk. The best long-term decision also depends on the time span and the returns over time.

Taking the first step to understanding whether or not a property is financially stable involves understanding that some properties will generate cash flow. However, others may require consistent or occasional out-of-pocket support. A property that requires constant out-of-pocket support can create stress, force rushed decisions, and consume a great deal of time.

Ignoring affordability can create stress, which will lead to reactive decisions and potential premature asset liquidation. Clear affordability thresholds allow investors to proceed more confidently in terms of deeper return analysis.

Why Does IRR Matter More Than Cash Flow When Comparing Renting vs Selling?

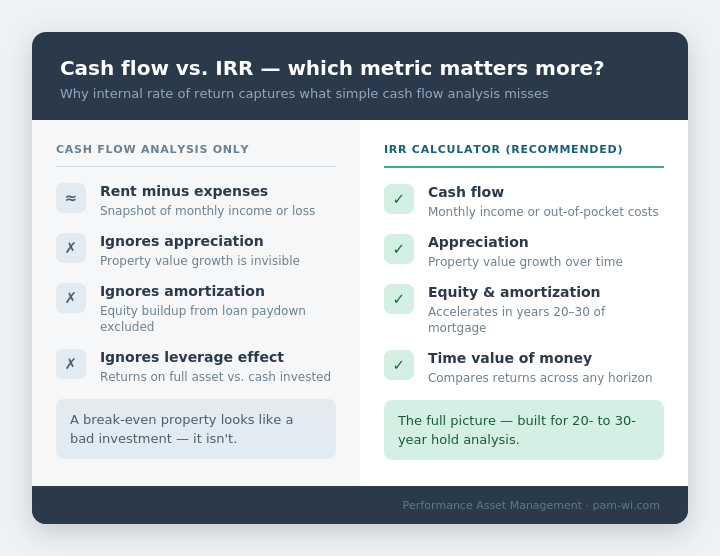

The mistake that many property owners make involves focusing on cash flow without examining the total investment performance over time. In short, comparing the sale price and rent returns oversimplifies complex investment decisions.

Many owners mistakenly judge a rental only by monthly cash flow. But professional real estate investment analysis evaluates property performance through multiple factors simultaneously:

Appreciation

Mortgage paydown

Tax advantages

Leverage

Rental income

Instead of taking the route to only consider rent and expenses to estimate rental property ROI, use an Internal Rate of Return (IRR) Calculator. The Internal Rate of Return incorporates appreciation, equity growth, cash flow, and time. IRR captures the full financial picture, making it the most important metric for long-term decisions.

This tool works particularly well for Southeastern Wisconsin residents, because applying an IRR Calculator works well in this area where there is a steady population base, consistent rental demand, and historically stable home appreciation rates. When combined, these factors make for an ideal 20- to 30-year hold strategy, which is exactly what IRR analysis is built for.

Even properties that break even can generate long-term returns, but this happens through leverage appreciation and amortization. Real estate lets investors control large assets with relatively small initial capital investment. But over time, compounding effects significantly increase total return beyond what cash flow suggests.

How Do Time Horizon, Debt Structure, and Market Conditions Affect ROI?

Longer timelines and favorable debt structures significantly increase the likelihood that renting outperforms selling.

Renting and selling each produce different return profiles. Another misconception that investors make involves underestimating how holding property compounds wealth through appreciation and debt paydown. Again, a structured framework helps with making this decision, as the first step is understanding whether a property is financially suitable for monthly rental.

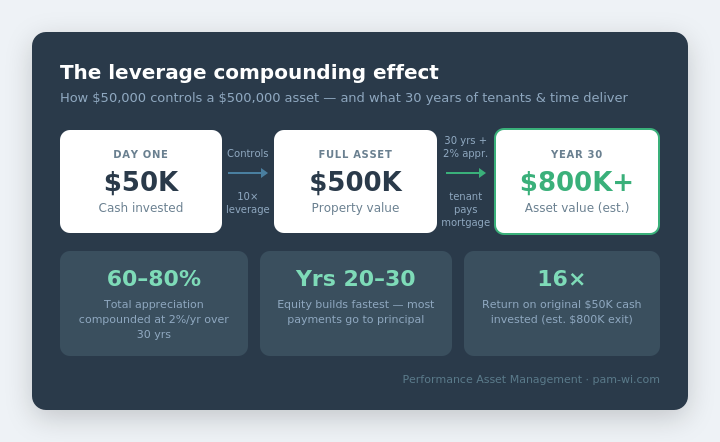

In short, the leverage and time do the heavy lifting. For some investors, this can feel abstract, unless they look under the hood. Take the following example:

Purchase price: $500,000

Down payment or cash invested upfront: $50,000

At this stage, the investor controls a $500,000 asset with $50,000. Moving forward, returns are based on the full value of the asset, not just the cash, unlike stocks or an IRA.

Even if the property never appreciates, after 30 years, the investor has transformed $50,000 into a $500,000 asset, with the tenant effectively paying the mortgage over time.

In reality, appreciation amplifies the outcome. Using a conservative appreciation assumption of 2% annually, which is well below the long-term growth trends reflected in the FHFA House Price Index, even modest appreciation compounds significantly over a 30-year hold period:

At a conservative 2% annual appreciation rate, a $500,000 property could grow to roughly $900,000 over a 30-year period before accounting for rental income and amortization benefits.

Using a more conservative working estimate of $800,000 to account for market variability, the $50,000 investment still represents a 16x return on the original cash invested, with a tenant funding the mortgage throughout

The $50,000 investment grew into an asset worth $800,000, generating rental income throughout the process.

In short, investors are using $50,000 to control a $500,000 asset, and over 30 years, their tenant and time work together to turn that into a fully paid-off asset worth several times the original investment. This is unlike a 401(k), where, instead of just contributing, investors are amplifying capital with debt and time.

Mortgage amortization also plays a major role in long-term ROI. Early mortgage payments are weighted heavily toward interest, while later payments shift toward principal reduction, significantly accelerating equity accumulation over time, according to the Consumer Financial Protection Bureau.

When Does It Make More Sense to Sell, Instead of Renting Your Property?

Selling makes sense when affordability is constrained, or better opportunities clearly outperform holding.

Despite the long-term benefits, transaction costs, which include commissions, transfer taxes, title fees, and repairs, typically reduce seller proceeds by roughly 6–10% of the sale price, according to a 2025 Redfin article.

Tax implications may also apply. For example, an investor selling a $500,000 rental property purchased for $300,000 could owe federal capital gains tax on the full $200,000 gain, potentially $30,000 or more, if the property was never used as a primary residence under the IRS Section 121 exclusion.

That liability factors directly into whether selling actually outperforms holding. Strong seller markets can also create opportunities to exit at favorable pricing conditions.

Ready to Run the Numbers? Compare Renting vs. Selling for Your Property

For those who have finished this article, you should now have a framework for evaluating renting or selling a property, in terms of which choice delivers stronger ROI. After individually reviewing affordability and long-term potential, it becomes easier to move with greater clarity and confidence. At that stage, the difference between outcomes can be substantial.

If you are an investor, deciding between renting and selling heavily impacts your retirement timelines, portfolio growth, and financial flexibility. Small differences in assumptions can have a significant impact on results when evaluating a 20–30-year horizon. This is why taking the time to carefully model scenarios can be a valuable step.

To move forward, run both the affordability and IRR Calculation scenarios based on your specific property. Understand realistic rent ranges, expense assumptions, and your comfort level with monthly cash flow. If you want someone to look over your numbers, connect with a PAM expert and walk through those scenarios together.