Why Did PAM Build Its Own Resident Screening Checklist?

Picture a successful southeastern-Wisconsin-based couple who regularly take four vacations a year, applying for about a $650 increase per month in rent at a higher-end unit. Their property manager wrote: "You're approved but consider renting something cheaper." The unthinkable happened: a property manager talked a qualified applicant out of renting something more.

The couple had liquid assets just above the threshold: the annual burden of the increase would be about $7,800 more, and their liquid assets were just above $10,000. In response, the couple sent Performance Asset Management (PAM) a thank-you letter for their message and continued living at their same means while traveling the world. All property managers screen residents—the real question is how.

After 17 years of working with thousands of residents, PAM developed its formula. And that resident screening checklist is the reason for the 99.5% eviction avoidance rate. It was built by reverse-engineering actual placement failures and reviewing that data. This article walks investors through every step of that checklist and the predictive metrics that drive it.

Why Did PAM Build Its Own Resident Screening Checklist?

PAM built its resident screening checklist by analyzing every failed placement and identifying affordability as the primary driver of defaults to identify affordability risk.

A 99.5% eviction avoidance rate across 200 placements means fewer than 1 in 200 residents need to go through a formal eviction process. The less-than-1% eviction rate excludes lease breaks caused by life events, such as job transfers, new family additions, or relationship changes. Failed placements are generally caused by affordability issues

The top reason that tenants miss rent payments is due to financial hardship, according to the Consumer Financial Protection Bureau (CFPB). And the Urban Institute has published research on eviction drivers showing income instability and rent burden as primary causes.

Because affordability is different from life cycle events, PAM designed its checklist to catch when this could be a problem. The goal was to create a predictive model that identifies affordability problems before they become evictions, and the current system does just that.

What Does PAM's Resident Screening Checklist Actually Verify?

PAM's resident screening checklist verifies eight factors using third-party sources: identity, Wisconsin court records, national court records, net income against bank deposits, liquid assets, employment tenure, rent payment history, and a full credit report.

The checklist runs eight verification steps, though three carry the most predictive weight: 24-month rental payment history, verified net income, and bank account balance. Read why in our article: How PAM Measures Resident Placement Success. The eight steps are as follows:

Identity: corroborate that the applicant is the person they claim to be

Wisconsin CCAP: search Wisconsin-based civil and criminal court records

National CCAP: view court records outside of Wisconsin on a national level

Income: verify net monthly income against actual bank deposits, not just pay stubs

Liquid assets: confirm their verified bank balance

Employment: review job tenure and industry stability for forward-looking indicators

Rent history: corroborate on-time payment records at the current residence

Credit: run a full credit report as the final data layer

Former landlords are removed from the eight-step process because a landlord trying to distance themselves from a difficult resident has every incentive to give a favorable reference. PAM replaced landlord references with third-party data that applicants cannot influence. In the end, the eight steps produce a weighted score, and no one factor approves or disqualifies an applicant.

What Two Metrics Best Predict if a Resident Will Default on Rent?

Liquid assets relative to the annual rent increase and a real-expense affordability check that measures what remains after rent, utilities, and fixed costs against verified net income are the two best predictors of affordability for residents.

Liquid assets vs. annual rent increase

After studying failed placements, PAM created a formula to predict rent default:

(New Rent − Current Rent) × 12

This calculates the additional financial burden the resident will absorb in year one

For example, a resident moving from $1,100/month to $1,500/month faces a $400 monthly increase, which is $4,800 annually

Residents with liquid assets above that threshold have a significantly higher success rate. This is because there’s a financial buffer able to absorb this life change. Without that buffer, one unexpected expense can trigger a debt spiral. Most importantly, this metric is verified against actual bank balances rather than just relying on the information provided by the applicant.

Because liquid assets measure whether a resident can absorb a one-time shock, the second metric measures whether their monthly budget was ever sustainable to begin with.

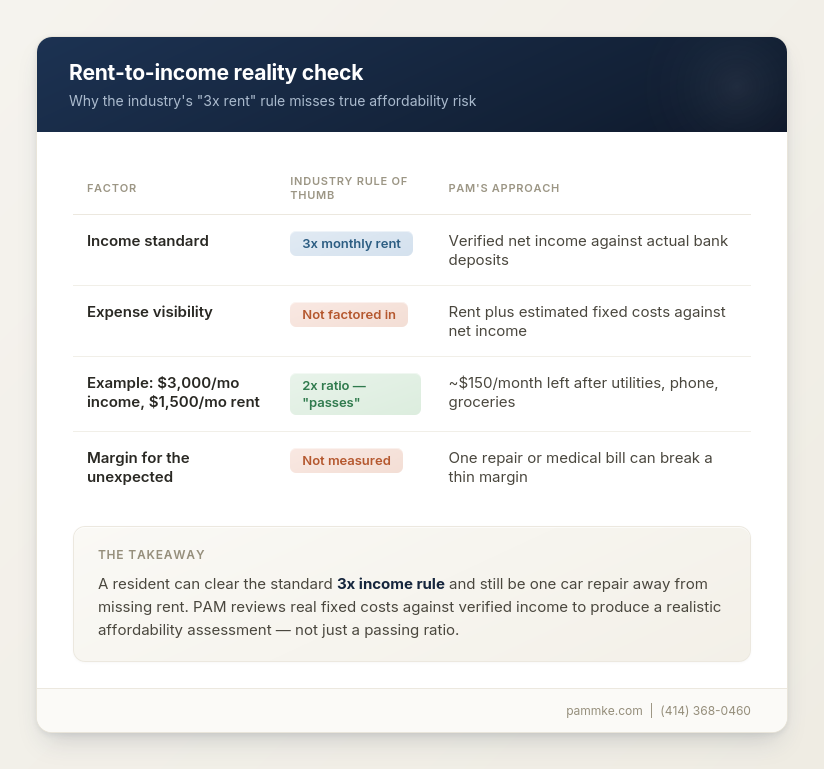

Rent-to-income reality check

The general guideline in the rental industry states that the income of the resident should be three times their rent. However, this idea doesn’t take actual living expenses into account. For example:

A resident earning $3,000/month net in a $1,500/month unit has a 2x ratio.

That leaves roughly $150/month left after utilities, phone, and groceries.

Working from a margin that thin means one expensive car repair or pricey medical bill could cause a real problem. PAM reviews the math: rent plus estimated fixed costs against verified net income. In the end, the result is a realistic affordability assessment that works in favor of the investor.

Why Does PAM Screen Residents This Carefully?

PAM guarantees that if a resident defaults, it will cover the eviction and re-leasing costs, meaning PAM only profits when rent is collected. That financial alignment makes rigorous screening a business necessity.

Failed placements are a direct loss that both PAM and the investor experience. This makes rigorous screening part of our business model, as it supports attracting quality residents who resign, protecting the NOI of our investors.

Alternatively, competitors with low placement fees that use a weak screening process and charge add-on protection fees help them profit from losses that investors and residents experience.

Why Does the PAM Checklist Matter to Investors Screening Managers?

The PAM screening checklist is a standard that investors can use to evaluate any potential managers to reveal whether a real screening process is in place.

Simply follow the eight steps and be sure to confirm that managers verify income against bank deposits, run national court records, and find out their eviction rate (plus how they define it). Also ask about their vacancy reduction process. A manager who screens well but takes months to fill a unit is only solving half the problem. The answers to these questions will reveal whether screening standards are in place as opposed to a compliance exercise.

If you’re an investor who is ready to see how PAM’s screening process compares to what you’re experiencing, take the next step. Have a conversation with Jim and go through the process together. Get your questions answered and find out more about screening residents.